From churches to youth organizations to the local chambers of commerce, nonprofit organizations make our communities more livable places. Unlike for-profit businesses that exist to generate profits for their owners, nonprofit organizations exist to pursue missions that address the needs of society. Nonprofit organizations serve in a variety of sectors, such as religious, education, health, social services, commerce, amateur sports clubs, and the arts.

Nonprofits do not have commercial owners and must rely on funds from contributions, membership dues, program revenues, fundraising events, public and private grants, and investment income.

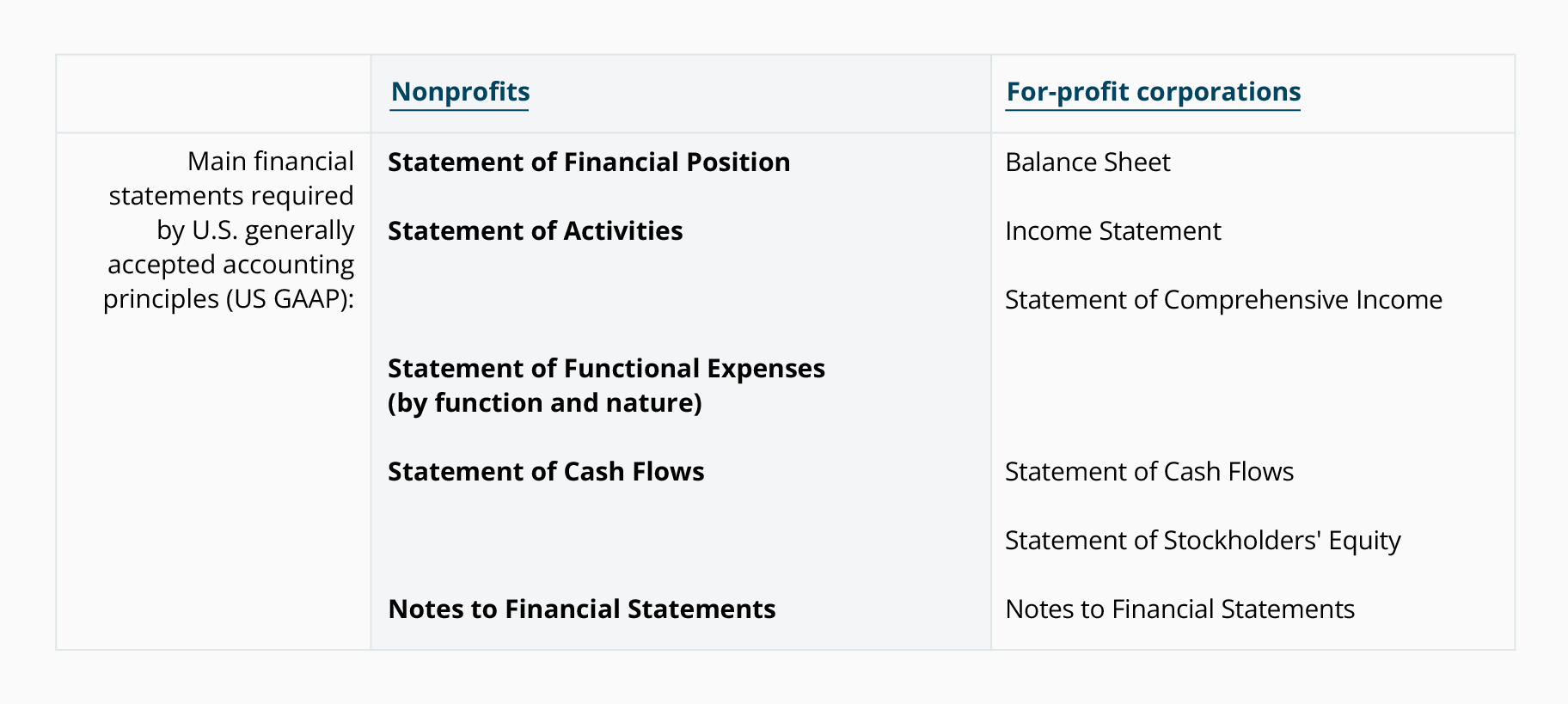

Our intent is to present some of the basic concepts that are unique to nonprofit accounting and reporting, including the financial statements required by the Financial Accounting Standards Board (FASB).