NOTE: In the following examples we assume that the employee's tax rate for Social Security is 6.2% and that the employer's tax rate is 6.2%. (During the years 2011 and 2012 only, the employee's rate was reduced to 4.2%.)

In this section of payroll accounting we will provide examples of the journal entries for recording the gross amount of wages, payroll withholdings, and employer costs related to payroll.

Let's assume that a distributor has hourly-paid employees working in two departments: delivery and warehouse. The company's workweek is Sunday through Saturday and paychecks are dated and distributed on the Thursday following the workweek.

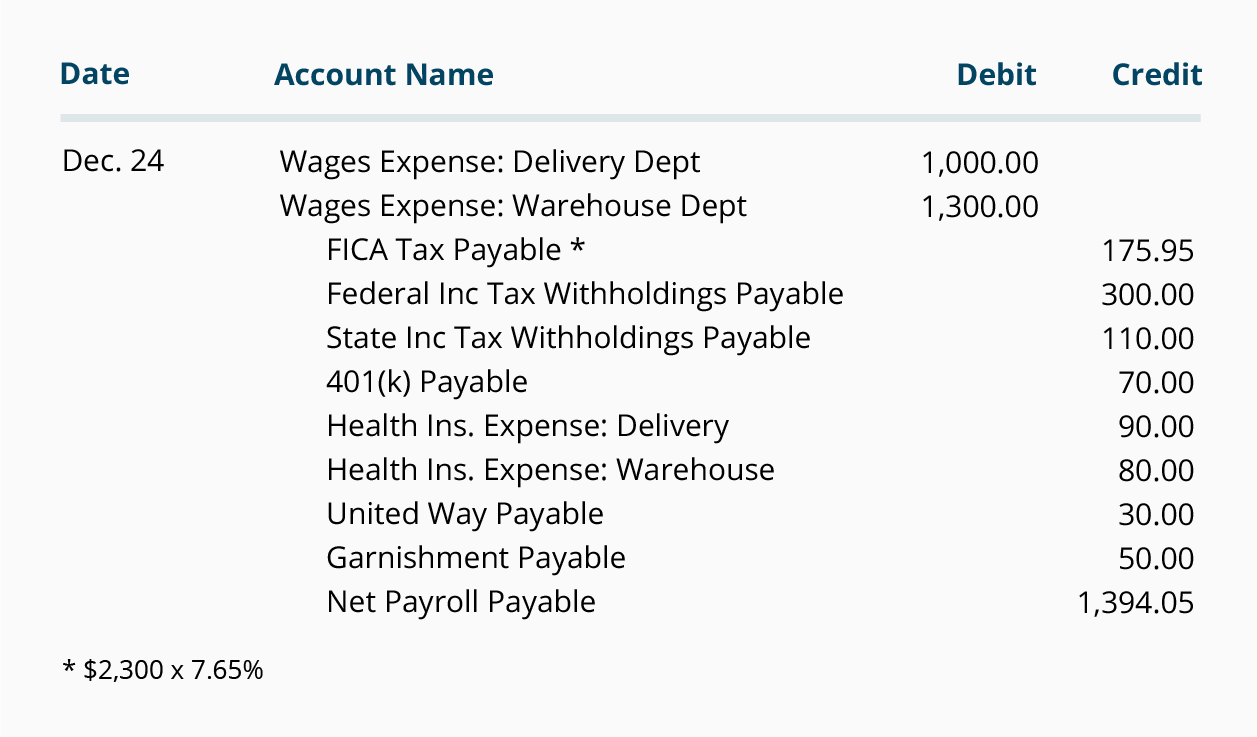

For the workweek of December 18-24, the gross wages are $1,000 for hourly employees in the delivery department and $1,300 for employees in the warehouse. Tax withholdings are determined by consulting government payroll guidelines; other withholdings are based on agreements with employees and court orders. Paychecks are dated and distributed on December 29.

The journal entry to record the hourly payroll's wages and withholdings for the work period of December 18-24 is illustrated in Hourly Payroll Entry #1. In accordance with accrual accounting and the matching principle, the date used to record the hourly payroll is the last day of the work period.

Hourly Payroll Entry #1: To record hourly-paid employees' wages and withholdings for the workweek of December 18-24 that will be paid on December 29.

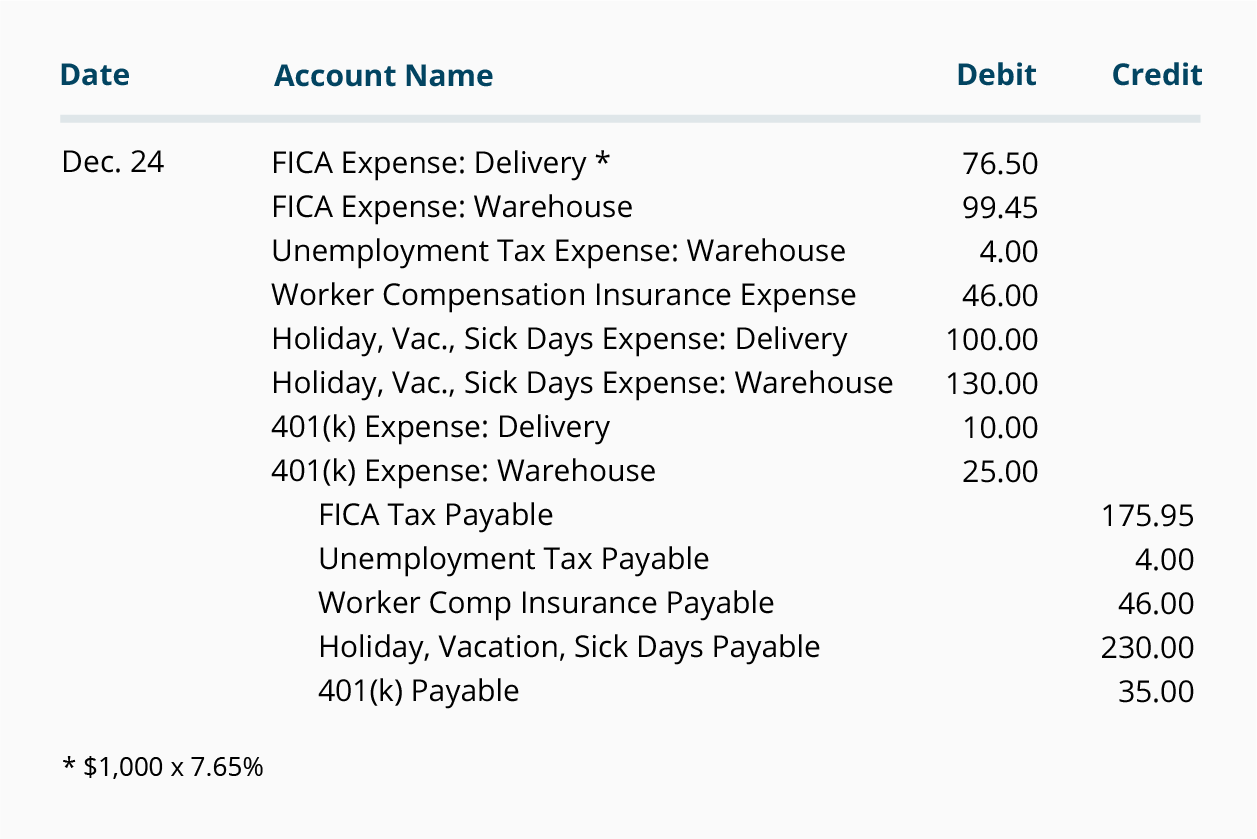

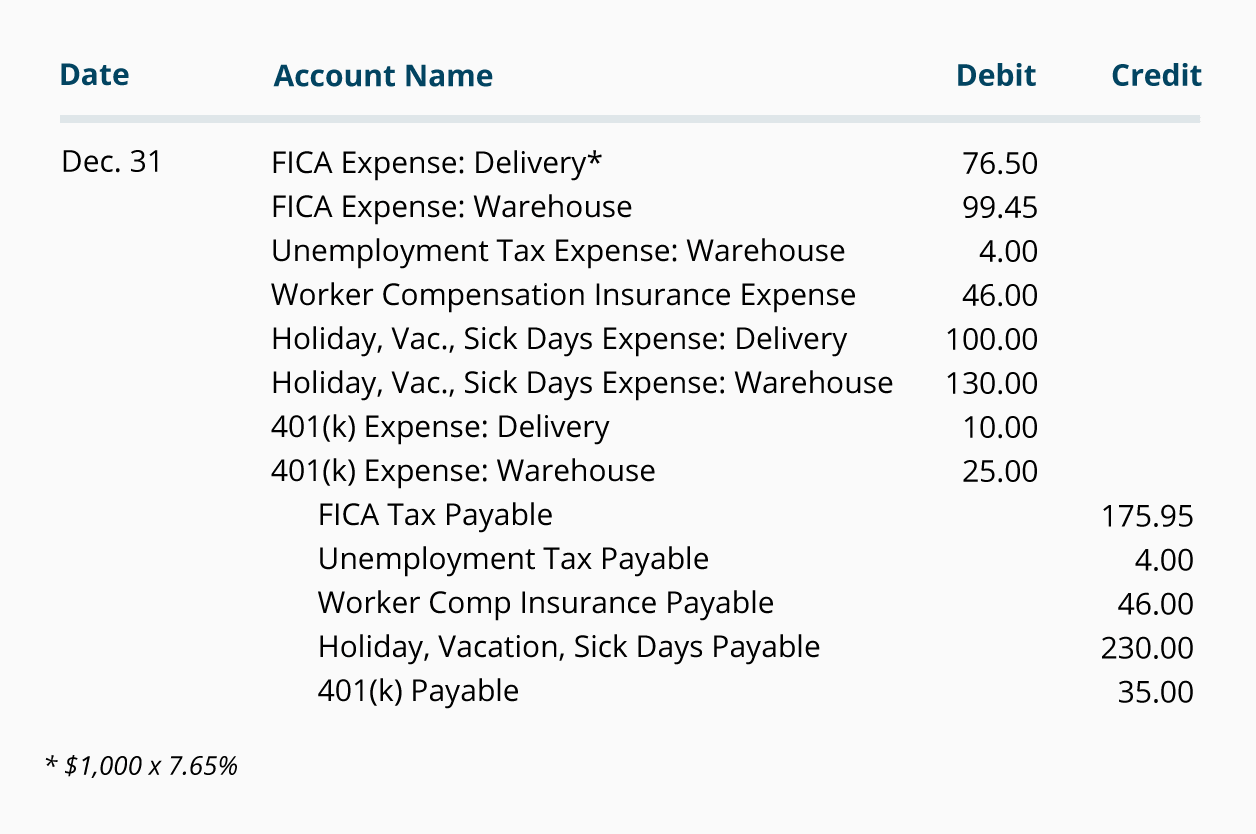

In addition to the wages and withholdings in the above entry, the employer has incurred additional expenses that pertain to the above workweek. These are shown next in Hourly Payroll Entry #2, which is also dated the last day of the work period. The items included are the employer's share of FICA, the employer's estimated cost for unemployment tax, worker compensation insurance, compensated absences, and company contributions for the company's 401(k) plan. The company is recognizing these additional expenses and the related liability in the period in which the employees are working and earning them. Later, when the company pays for them, it will reduce the liability and reduce its cash. (Our journal entry assumes that this company does not provide post-retirement benefits—like pensions or health insurance—to its employees.)

Hourly Payroll Entry #2: To record the company's additional payroll-related expense for hourly-paid employees for the workweek of December 18-24.

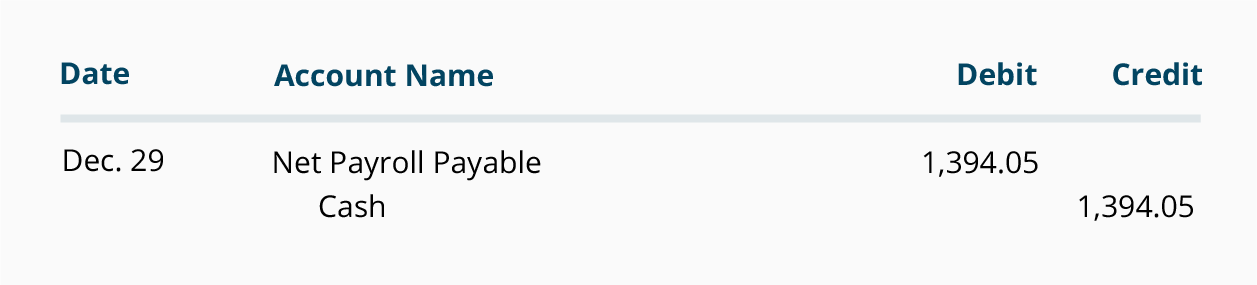

On payday, December 29, the checks will be distributed to the hourly-paid employees. The following entry will record the issuance of those payroll checks.

Hourly Payroll Entry #3: To record the distribution of the hourly-paid employees' payroll checks on Dec. 29. (These checks reflect the net pay for the wages earned during the workweek of Dec. 18-24).

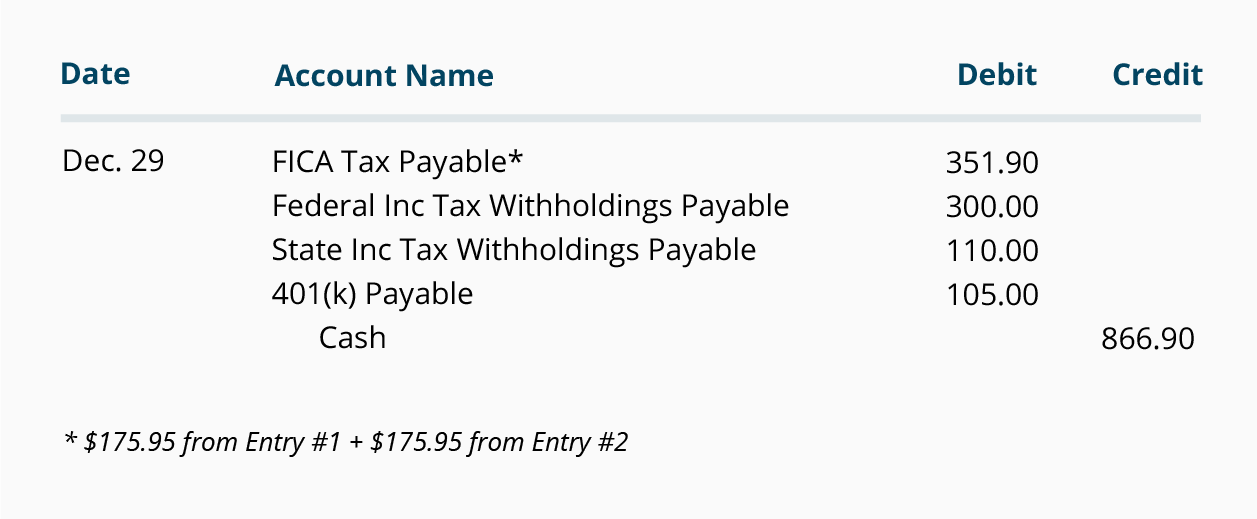

Some withholdings and the employer's portion of FICA were remitted on payday; others are not due until a later date. Some withholdings, such as health insurance, were recorded as reductions of the company's expenses in Hourly Payroll Entry #1. We will assume the amounts in the following Hourly Payroll Entry #4 were remitted on payday.

Hourly Payroll Entry #4: To record the remittance of some of the payroll withholdings and company matching pertaining to the hourly-paid workweek of Dec. 18-24.

End of Month and End of Year

Let's continue with our example of the payroll for the hourly-paid employees. We'll assume that this distributor's accounting month and accounting year both end on Saturday, December 31. The

matching principle requires the company to report all of its December

expenses (not simply its cash payments) on its December financial statements. This means the company must report on its income statement the hourly wages and other payroll expenses that the company incurred (and the employees earned) through December 31.

Recall that the paychecks issued on December 29 covered the work done by hourly employees through December 24. The company must now record the cost of work done during the week of December 25-31 (a week that includes a Christmas holiday plus a number of employees taking vacation days).

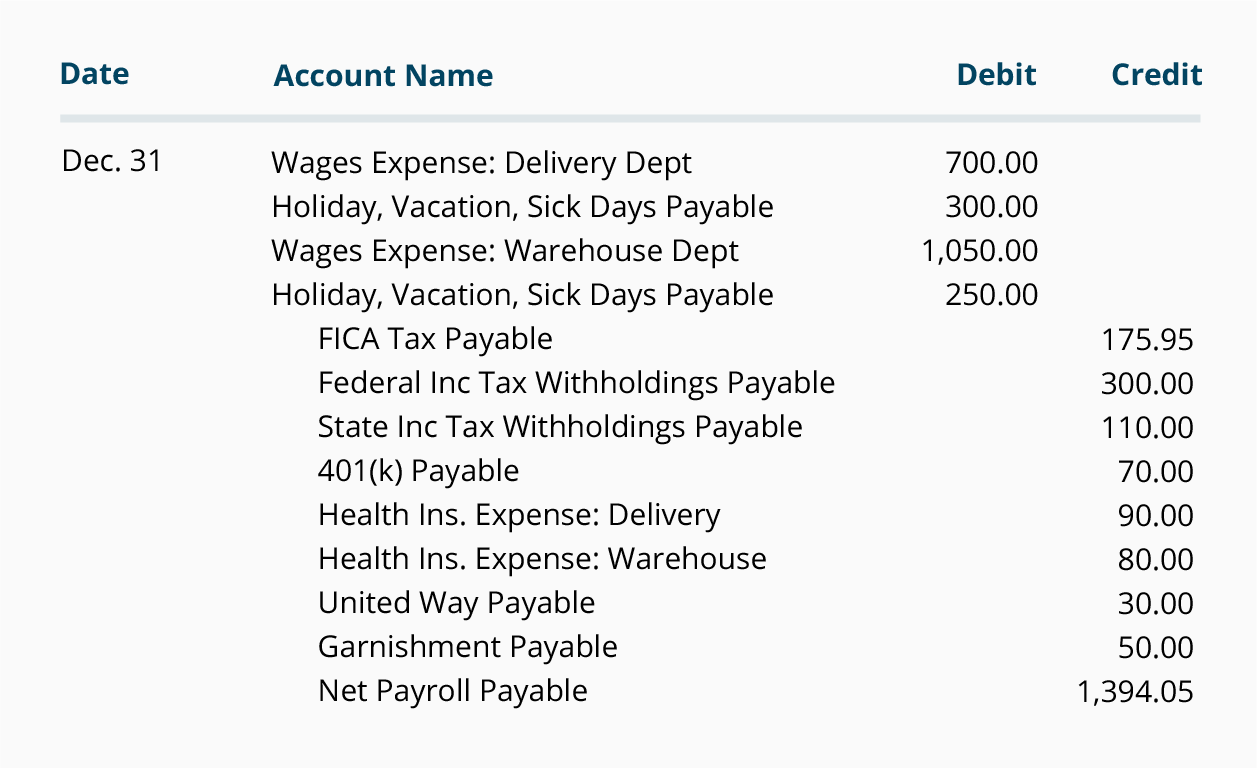

Let's assume that during the workweek of December 25-31, delivery department employees took $300 worth of their holiday and vacation days. Since a portion of the employer's estimated cost of holiday and vacation days was recorded as an expense and liability via each week's Hourly Payroll Entry #2, the $300 associated with the days actually taken this week will not be recorded as an expense—rather, the $300 associated with the days taken this week will reduce the liability that is recorded with each week's Hourly Payroll Entry #2. In other words, only $700 of the delivery department's employee gross wages of $1,000 is for the work performed this week. The warehouse department had a similar situation. Of the warehouse department's $1,300 of weekly wages, only $1,050 is the expense for the work performed this week. The wages associated with the "days off with pay" reduces the company's liability that was provided for each week in Hourly Payroll Entry #2. Except for the holiday and vacation days, the workweek payroll for December 25-31 is similar to the previous week.

Hourly Payroll Entry #1: To record hourly-paid employees' wages and withholdings for the workweek of December 25-31 that will be paid on January 5.

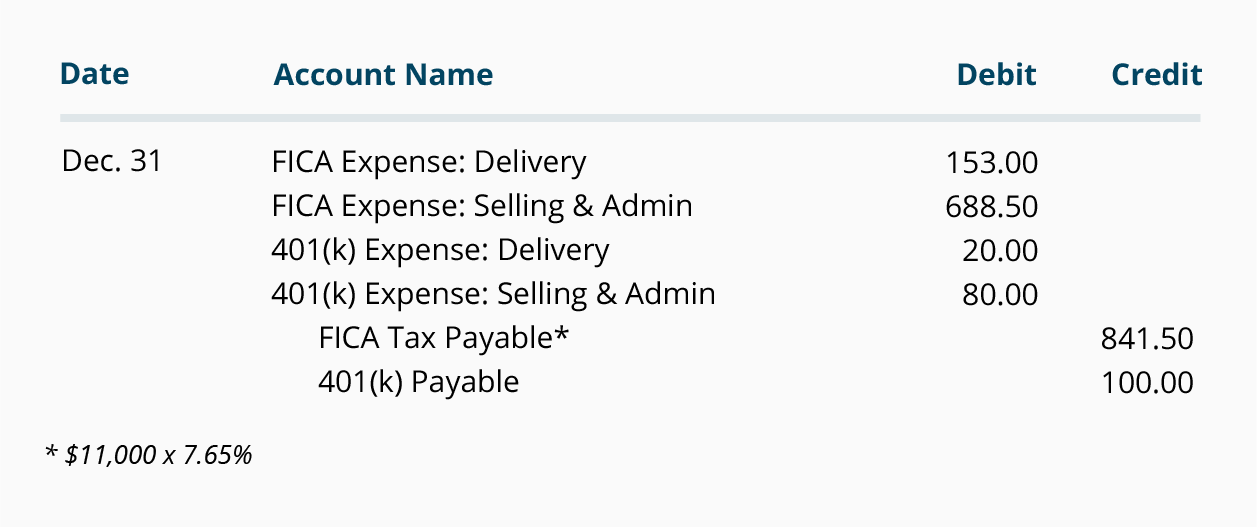

In addition to the wages and withholdings in Hourly Payroll Entry #1, the employer has incurred additional expenses that pertain to the above workweek. These are shown next in Hourly Payroll Entry #2, which is also dated the last day of the work period. The items included are the employer's share of FICA, the employer's estimated cost for unemployment tax, worker compensation insurance, compensated absences, and company contributions for the company's 401(k) plan. The company is recognizing these additional expenses and the related liability in the period in which the employees are working and earning them. Later, when the company pays for them, it will reduce the liability and reduce its cash. (Our journal entry assumes that this company does not provide post-retirement benefits-like pensions or health insurance-to its employees.)

Hourly Payroll Entry #2: To record the company's additional payroll-related expense for hourly-paid employees for the workweek of December 25-31.

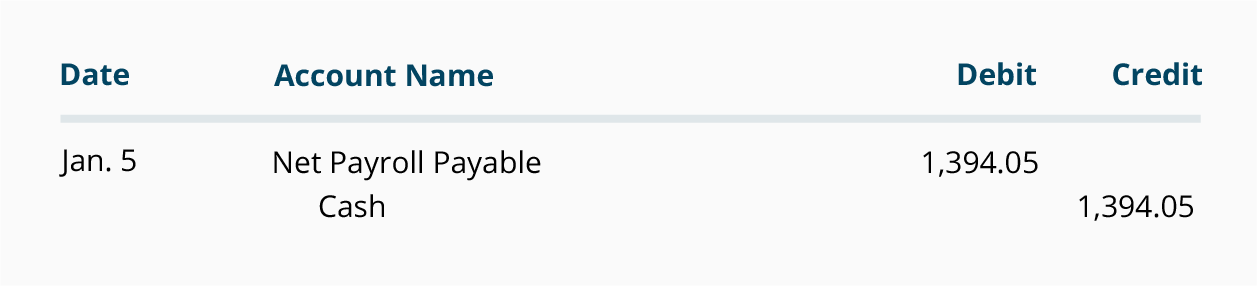

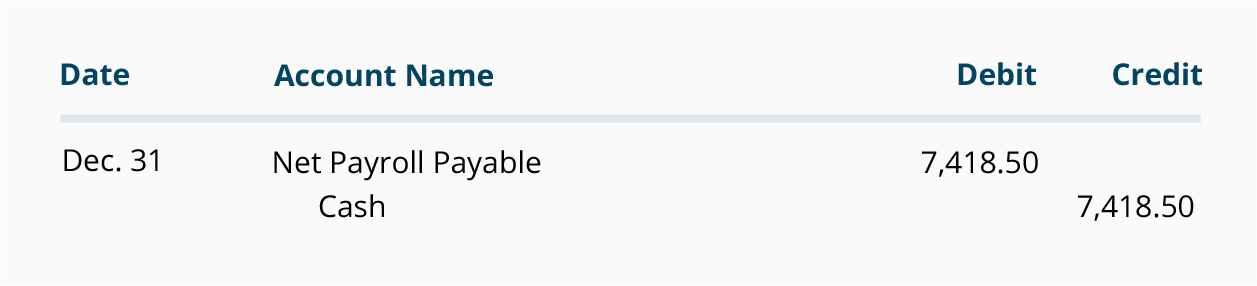

On payday, January 5, the checks will be distributed to the hourly-paid employees. The following entry will record the issuance of those payroll checks.

Hourly Payroll Entry #3: To record the distribution of the hourly-paid employees' payroll checks on Jan 5. (These checks reflect the hourly-paid employees' take home pay from their wages earned during the workweek of Dec. 25-31).

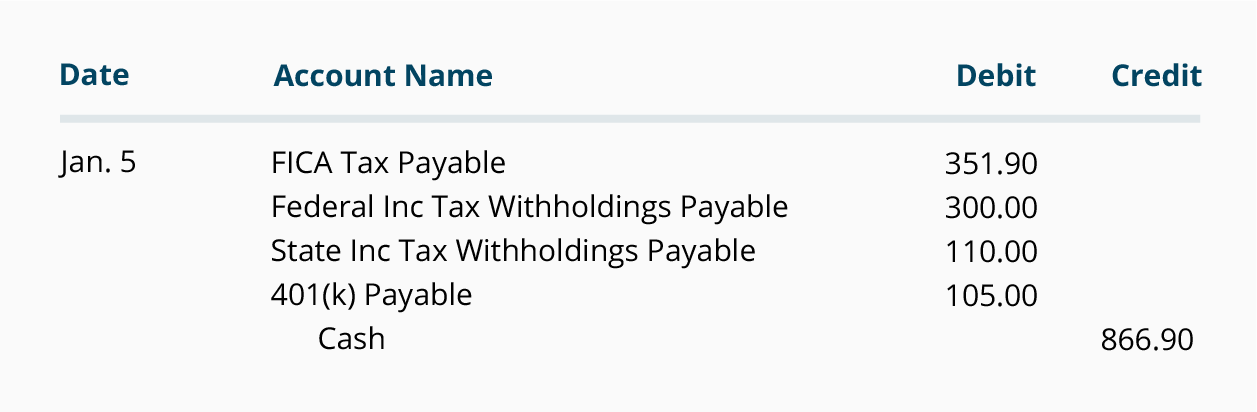

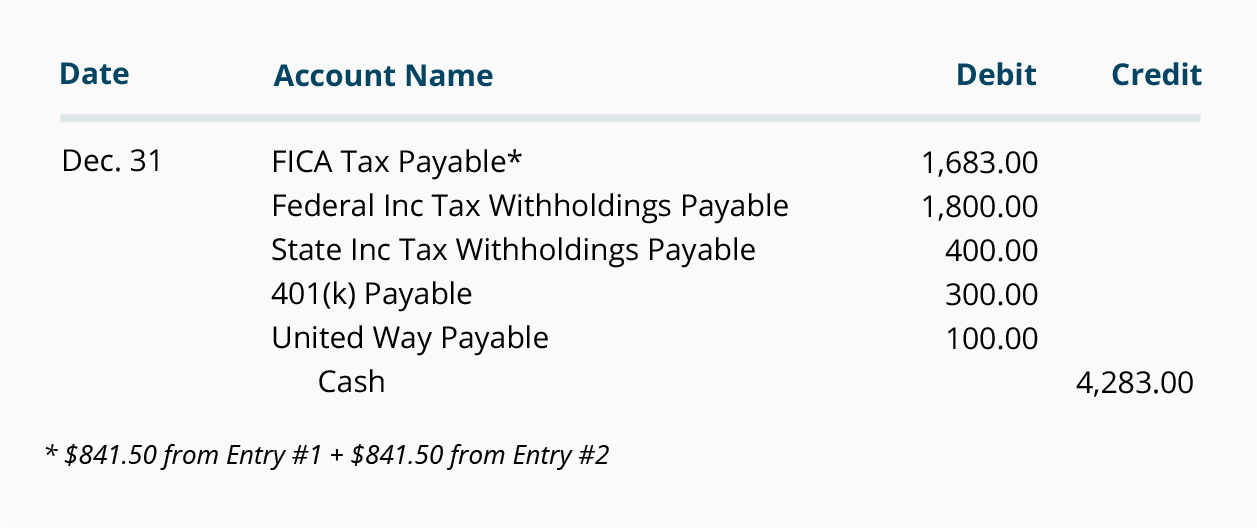

Some withholdings and the employer's portion of FICA were remitted on payday; others are not due until a later date. Some withholdings, such as health insurance, were recorded as reductions of the company's expenses in Hourly Payroll Entry #1. We will assume the amounts in the following Payroll Entry #4 were remitted on payday.

Hourly Payroll Entry #4: To record the remittance of some of the payroll withholdings and company matching pertaining to the hourly-paid workweek of Dec. 25-31.

Additional Accrual of Wages

In our example above, the workweek ended on the same day as the calendar month and year: December 31. In other months and in some years, the last full workweek might end on the 28th of the month. In that case, the employer will need to estimate the payroll and payroll-related expenses for the 29th, 30th, and 31st days of the month. Those estimates will be used to record an

accrual-type adjusting entry on the 31st. This is required so that all of the expenses actually occurring during the month are matched with the revenues of the month. Recording wages expense in the proper period is critical for accurate financial statements and therefore a very important part of payroll accounting.